How Fed Rate Cuts Could Trigger A Melt-up, Followed By A Crash?

As the US economy slows down and very likely heads towards a recession, equity markets around the world face the prospects of a large draw-down of the sorts that has historically been witnessed around the time of the onset of a recession in the US.

However, the path to any such correction very likely first passes through a strong rally in equity markets that is underway right now, which if anything, is likely to accelerate even further once the Fed start cutting Fed Funds Rate (FFR), and this in turn presents an once-in-a-cycle opportunity to create wealth for investors in the near future by participating the final stages of the melt-up in equity markets that is likely to be triggered once the Fed actually starts cutting rates for the current cycle.

The great slowdown is underway!

The most important macro-economic trend gaining strength right now is the unmistakable slowdown being witnessed in the US economy. This is, of course getting overshadowed for the time being by a roaring stock market driven by a handful of AI-mania gripped stocks such as NVDIA etc.

But the signs of a slowdown in the “real” economy are getting louder by the day. Unemployment rate is now up at 4% from a cycle low of 3.5% as of a year back. One after another, consumer facing companies from Starbucks, McDonald’s and Target are reporting slowing demand for their goods and services. Even tech behemoths like Salesforce have now joined the bandwagon by recently reporting a weak outlook for demand of their goods and services.

What do fed rate cuts mean for equity markets?

As the effects of this slowdown become more and more apparent, it will ultimately force the Federal Reserve to act and initiate rate cuts.

And history shows that rate cuts, as and when they start, are at least initially, interpreted by equity markets to mean that cost of capital for both consumers and businesses would start to come down. Hence the start of fed rate cuts has historically been treated by equity markets as a very bullish signal for stocks and is usually marked by acceleration in the on-going rally in equity markets.

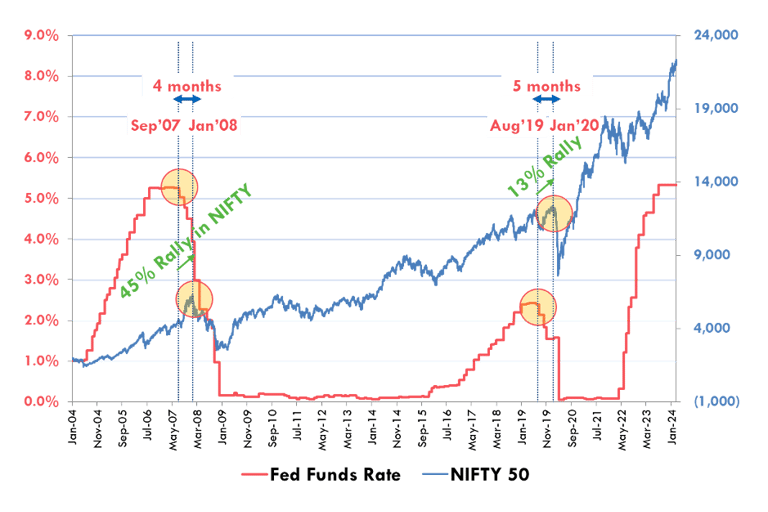

In India, the start of rate cuts in the US has historically triggered the most violent part of melt-up - the NIFTY rallied an impressive 13% in just about 5 months the last time the Fed started cutting rates in Aug 2019. And in the cycle prior cycle to that, the NIFTY rallied an even more spectacular 45% in just 4 months after the Fed started cutting rates around Sept 2007.

Exhibit 1: Historically, start of fed rate cuts have triggered the most violent part of the melt-up in the NIFTY-50

We are now at the cusp of yet another rate cut cycle and this in turn presents an once-in-a-cycle opportunity to create wealth for investors in the near future by participating the final stage of the melt-up in equity markets that is likely to be triggered once the Fed actually starts cutting rates for the current cycle.

But it always ends in disaster!

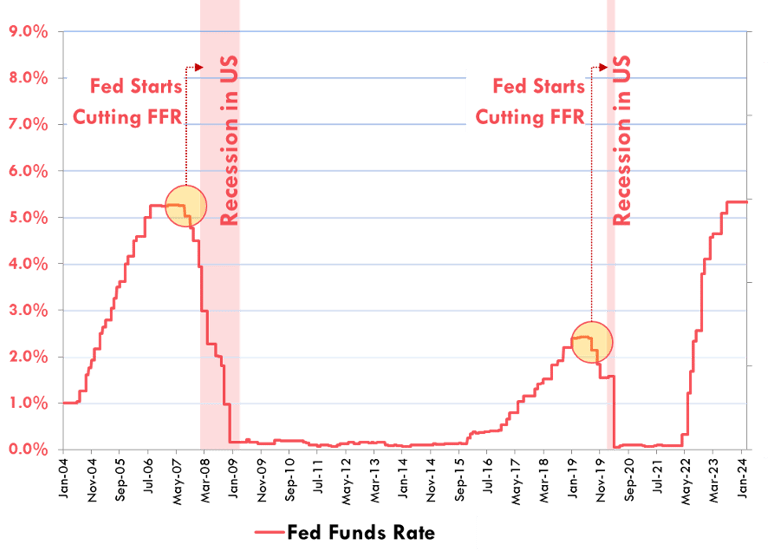

However, notwithstanding the exuberance that grips equity markets as we head towards the start of fed rate cuts, it is absolutely critical to be conscious at all times that such exuberance is absolutely unwarranted, and that history is very clear on this – the real reason the Fed has to start cutting rates towards the end of every business cycle is NOT because it really intends to pander to equity markets, but because economy is in such a bad state and demand slowdown so severe that the Fed simply has no option left by then but to cut rates, in the hope that rate cuts would be able to salvage the economy and prevent it from slipping into a recession.

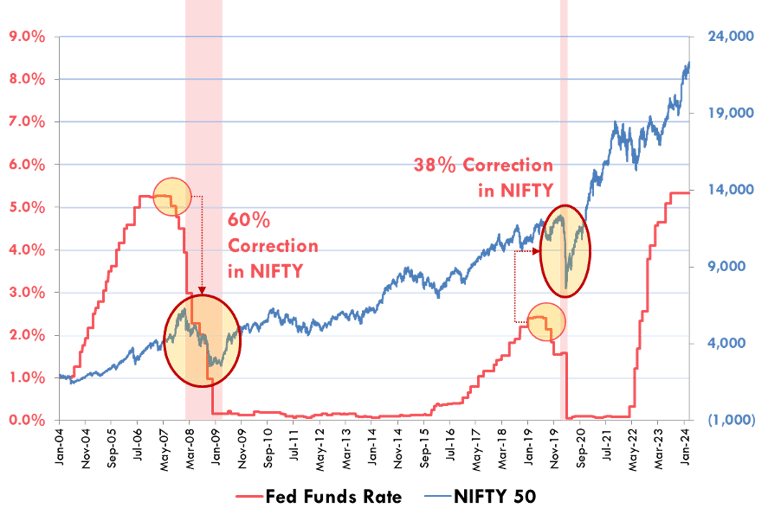

Exhibit 2: Historically, the US economy has slipped into a recession anyways, despite the Fed starting to cut rates

And yet history shows that Fed has hardly ever been successful in this, and that the US economy has slipped into a recession anyways, despite the Fed cutting rates, and that too within just 4-5 months of the Fed starting to cut rates.

And as the economy sinks eventually, so do equity markets!

Not just that, historically, recessions in the US have also been marked by steep stock market corrections, NOT just in the US, but pretty much around the world including here in India. Hence, as equity markets every time realize the hard way, there is absolutely nothing to cheer about Fed starting to cut rates, and that any rally in stocks that ensues after Fed starts to cut rates fizzles out pretty soon and in fact paves the way for a large drawdowns in equity markets once the economy actually slips into a recession.

In India, the NIFTY corrected by 38% after the US economy slipped into a recession the last time after the onset of the COVID pandemic in March 2020. In the previous cycle, the NIFTY corrected by a whopping 60% - the highest in its history – once the US economy slipped into a recession from early 2008 onwards.

Exhibit 3: Historically, recessions in the US have invariably been marked by large equity market corrections in the NIFTY

Conclusion

While we are almost certainly headed for a large drawdown in equity markets once the US economy eventually slips into a recession, the path to any such correction very likely first passes through a strong rally in equity markets.

However participation in this last phase of the “melt-up” that typically kick-starts after the start of fed rate cuts in US must be undertaken without for a moment losing sight of the fact that such rallies have historically almost always fizzled out within 4-5 months of the Fed starting to cut rates, because the US economy has slipped into a recession anyways, despite the Fed cutting rates, and that too within just 4-5 months of the Fed starting to cut rates. And this is what in turn, has historically triggered large stock market corrections, both in the US as well as in here in India.

Disclaimer

This document is exclusively for educational purpose and anything contained herein should NOT be construed as investment advice. Equity market and/or mutual fund investments are subject to market risks. Also, while past precedence and trends in equity markets serve as useful reference, there is no guarantee that equity markets would necessarily trend in future in line with their past trends and behavior. Readers and subscribers are advised to seek independent professional advice and verify the contents of this document before making any actual investment. The authors of this document will NOT be responsible for any profit or loss arising directly or indirectly as a result of following and/or applying the contents of this document.

India's first global-macros driven hedge fund

Address: 307, Indiabulls MINT, Opposite Hiranandani Meadows, Manpada, Thane (West), Maharashtra - 400610 India

© 2026 – metacaps.ai is a registered trademark of ANIINCAPS PRIVATE LIMITED