Monthly Income Plan for Retirees: Beyond Fixed Income (2026)

When it comes to a monthly income plan for retirees in India, conventional wisdom has long suggested that as individuals approach retirement, they should steadily reduce equity exposure and move most of their savings into low-risk, fixed-income instruments. The reasoning seems logical—lower volatility, capital preservation, and predictable income.

However, this approach was designed for a very different era.

What Is a Monthly Income Plan for Retirees?

A monthly income plan for retirees is a structured investment strategy designed to generate regular monthly cash flow after retirement, while also aiming to preserve capital and protect purchasing power against inflation.

Unlike traditional fixed-income options that focus only on stability, a well-designed monthly income plan balances income generation, inflation protection, and long-term sustainability, especially for retirements that can last 25–30 years.

Why Monthly Income Plans Must Evolve for Modern Retirees

With rising life expectancy and advancements in healthcare, retirees today are living significantly longer than previous generations. Living into one’s late 80s or even 90s is no longer an exception. As a result, someone retiring at 60 may need monthly income for 25 to 30 years or more.

Over the last few decades, life expectancy in India has steadily increased due to improvements in healthcare and living standards. For many retirees today, planning for a post-retirement phase of 25 to 30 years is no longer conservative, it is increasingly realistic.

Over such extended periods, relying only on fixed-income and debt instruments creates a fundamental challenge: the inability to consistently beat inflation after taxes. When rising healthcare expenses and evolving lifestyle costs are factored in, the real purchasing power of a fixed-income-only portfolio can gradually erode.

Even relatively moderate long-term inflation can meaningfully reduce purchasing power over a multi-decade retirement period, making fixed-income-only strategies increasingly vulnerable over time.

Healthcare expenses tend to rise faster than general inflation, especially in later years, making retirement monthly income planning as much about adaptability as about predictability.

This highlights why post-retirement financial planning and inflation-adjusted retirement income strategies are more critical than ever.

Why Traditional Retirement Monthly Income Plans Fall Short in India

Most traditional monthly income plans in India are structured around fixed returns and guaranteed income models. While these products provide short-term comfort and stability, they often fall short when viewed through the lens of a long retirement horizon.

A purely fixed-income approach does little to address three critical retirement risks:

Long-term inflation - the rising cost of living can slowly erode the real value of fixed payouts

Rising medical and healthcare costs- medical and healthcare expenses tend to rise faster than general inflation

Longevity risk or the risk of outliving one’s savings - the chance of outliving your savings increases with longer life spans

Over a 20–30 year retirement period, even moderate inflation can significantly reduce real wealth. This structural limitation has created the need for a more adaptive post-retirement income strategy, one that balances income stability with long-term growth potential.

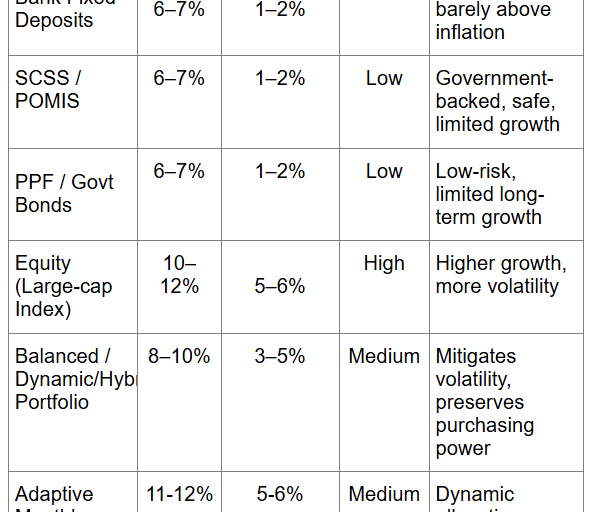

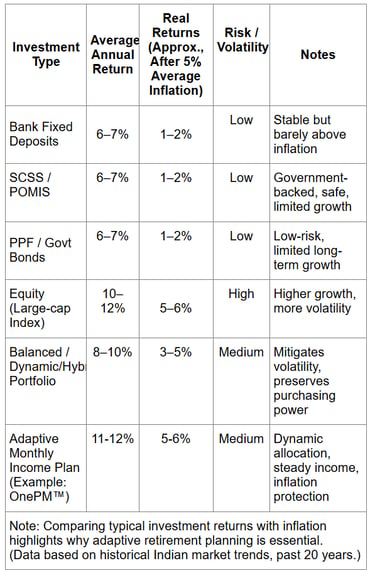

Real Returns vs Inflation: Why Fixed Income Alone Isn’t Enough for Retirees in India

To understand how our OnePM™ Plan continuously adjusts its exposure between equity and debt based on prevailing market liquidity conditions, please watch the YouTube video below

Why Equity Exposure Matters in Monthly Income Plans

Modern monthly income planning can no longer completely eliminate equity exposure. The objective is not to avoid equity, but to manage it intelligently and responsibly.

A carefully structured equity-debt allocation helps retirees maintain purchasing power over long post-retirement periods, provides growth potential to counteract inflation, and mitigates the risk of running out of funds during market downturns.

Controlled equity exposure helps offset inflation risk and supports income sustainability over long retirement horizons.

Risks and Limitations of Monthly Income Plans

While monthly income plans aim to provide stability and sustainable cash flow, it’s important to understand potential limitations:

No guaranteed returns: Market-linked strategies can fluctuate, and past performance does not guarantee future results.

Equity exposure risk: Although controlled exposure helps counter inflation, it introduces volatility, especially in the short term.

Time horizon requirement: Adaptive plans generally require a long investment horizon (often 5+ years) to smooth market upcycles and downturns.

Tax implications: Interest from fixed income and equity gains may be subject to taxation depending on individual profiles.

How the MetaCaps OnePM™ Monthly Income Plan Works

The MetaCaps OnePM™ Monthly Income Plan is designed as an adaptive income strategy, combining equity and debt exposure based on market conditions. The objective is to provide consistent monthly income while dynamically managing risk across different market cycles.

Designed for retirees and near-retirees seeking regular monthly income, the OnePM Plan moves away from static asset allocation and adopts a dynamic portfolio management framework.

Unlike conventional retirement products that maintain a fixed equity-debt mix regardless of market conditions, the OnePM Plan actively adjusts its allocation based on prevailing liquidity and risk environments.

When market liquidity tightens and risk levels rise, equity exposure is reduced to help protect capital.

When liquidity improves and risk eases, equity allocation is increased to participate in growth opportunities.

Retirement income strategies that fail to account for changing market cycles often struggle to maintain consistency during periods of tightening liquidity or elevated volatility.

This adaptive investment logic forms the core strength of the OnePM strategy. It is designed to support a forward-looking retirement portfolio strategy, retaining sufficient equity exposure for long-term inflation-adjusted retirement income while actively managing downside risk during unfavourable market phases.

Built for Monthly Income With Long-Term Stability

Historically, the MetaCaps OnePM Monthly Income Plan has been structured around two key objectives for investors who remain invested for at least five years:

To provide a steady, inflation-adjusted monthly income throughout the investment period.

To aim for capital preservation, allowing investors to recover their principal amount at the end of the five-year tenure.

It is important to note that this is not a guaranteed return product. However, based on historical performance analysis, investors who have stayed invested over a full market cycle have typically experienced consistent monthly payouts, even during challenging market environments, while also recovering their initial investment at maturity.

This illustrates how an adaptive monthly income strategy can help retirees achieve steady monthly income while managing risk and protecting against inflation.

Who Should Consider the MetaCaps OnePM™ Monthly Income Plan?

The OnePM Plan may be suitable for:

Retirees seeking regular monthly income while prioritising capital preservation

Individuals aged 50+ planning for a medium- to long-term investment horizon of five years or more

Investors looking for a smarter alternative to traditional fixed deposits, annuities, or income-focused debt products

Those aiming to protect their retirement corpus against inflation through a balanced, research-driven approach

This approach is best suited for retirees with a medium-to-long-term outlook who prioritize sustainability over short-term yield certainty.

Frequently Asked Questions (FAQs)

1. What is the best monthly income plan for retirees?

There is no one-size-fits-all plan. The best monthly income plan balances regular income, inflation protection, and long-term sustainability based on individual retirement needs.

2. Are fixed-income instruments enough for monthly income?

Fixed-income instruments — such as bank FDs, senior citizen schemes, and fixed pension payouts — may provide stability but often fail to keep up with inflation over long retirement horizons.

3. Why include growth assets in a monthly income plan?

Selective growth exposure, such as equities or hybrid strategies, helps protect the real value of income, offsetting inflation and rising expenses.

4. How long should one plan for monthly income?

With increasing life expectancy, planning for at least 25–30 years of income after retirement is increasingly realistic.

5. Can a monthly income plan preserve capital?

A well-structured strategy aims to preserve capital while providing stable income, but no investment — including adaptive monthly income plans — can guarantee returns.

Why Adaptive Monthly Income Plans Stand Out in India

By dynamically managing equity and debt exposure, the MetaCaps OnePM Plan strikes a careful balance between income stability and long-term capital protection. It allows retirees to benefit from selective equity participation without bearing the full volatility typically associated with equity markets.

For investors evaluating retirement monthly income plans in India, especially those looking for adaptability, risk management, and sustainable monthly income, the OnePM Monthly Income Plan represents a differentiated and forward-looking solution.

Key Takeaway

In an environment shaped by longer lifespans, persistent inflation, and rising healthcare costs, retirement planning can no longer rely solely on fixed-income strategies.

The MetaCaps OnePM™ strategy demonstrates an approach to monthly income planning, combining steady payouts, adaptive portfolio management, and capital preservation. For retirees seeking a resilient and well-structured approach to post-retirement income, it serves as an example of how adaptive strategies can support long-term financial stability.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Investors should consider their personal situation or consult a qualified advisor before making investment decisions.

India's first global-macros driven hedge fund

Address: 307, Indiabulls MINT, Opposite Hiranandani Meadows, Manpada, Thane (West), Maharashtra - 400610 India

© 2026 – metacaps.ai is a registered trademark of ANIINCAPS PRIVATE LIMITED